Cost-Benefit Analysis¶

What is the current value of a future sum? The answer to this question helps to decide whether an investment is worth the sacrifice.

Present Value of a Future Sum¶

We need to make an investment decision. We assume that any investment

requires sacrificing current resources, and

has an expected return.

Then the question is: Is the investment worth it?

The main tool to make investment decisions in a cost benefit analysis is a reverse interest calculation.

To introduce the present value of a future sum, consider the following two problems.

In ten years we will inherit \(\$100,000\). Assuming \(5\%\) rate with continuous compounding, how much can we borrow today?

The lottery (or an insurance settlement) offers

either to pay half of the prize \(p\) now, that is \(p/2\); or

installments of \(p/25\) for 25 years.

What should the interest rate be to break even?

To solve these two problems, we need to answer the following.

What is the present value of \(\$100,000\) in ten years?

What is the present value of receiving 25 yearly installments?

Let us do an example of a reverse interest calculation: What is the present value of \(\$3,000\) in five years, assuming an annual interest rate of \(8\%?\)

We can interpret the middle number in the above sequence in two ways:

The anser to the reverse interest question is then \(\$3,000 (1 + 0.08)^{-5} = \$2,042\), rounded to nearest \(\$\).

Let us return to the first problem, on borrowing against an inheritance: In ten years we will inherit \(\$100,000\). Assuming \(5\%\) rate with continuous compounding, how much can we borrow today?

We start with some notations:

\(t = 10\) is the number of years in the future.

\(P = 100000\) is value of the inheritance.

\(r = 0.05\) is the interest rate.

\(L\) is the amount of the loan.

With continuous interest compounding at rate \(r\), the loan amount \(L\) equals \(P\) after \(t\) years:

\(L = \$100,000 e^{-0.5} = \$60,653.07\) is the highest amount of the loan.

After these examples, we are ready to formulate the present value of future money.

We apply this formula to considering payout options. The lottery (or an insurance settlement) offers

either to pay half of the prize \(p\) now, that is \(p/2\); or

installments of \(p/25\) for 25 years.

What should the interest rate be to break even? What is the present value of the 25 installments? Let \(r\) be the interest rate, using continuous compounding:

We will arrive at a nonlinear equation. The sum of the 25 installments equals:

The alternative option is to receive a lump sum of \(p/2\). The break even point is defined by

which simplifies into

so the break even point does not depend on the prize \(p\).

Returning to the original question. The lottery (or an insurance settlement) offers

either to pay half of the prize \(p\) now, that is \(p/2\); or

installments of \(p/25\) for 25 years.

What should the interest rate be to break even?

Solving the nonlinear equation with NLsolve package in Julia

leads to the break even rate of \(6.74\%\).

Naturally, the higher the interest rate, the smaller the present value of the future money.

The Julia package NLsolve provides a nonlinear solver,

its use to compute the break even rate is shown below:

using NLsolve

"""

function f!(F, x)

defines F[1] as the input to nlsolve.

"""

function f!(F, x)

r = x[1]

F[1] = 1 - exp(-25*r) - 12.5*(1 - exp(-r))

end

sol = nlsolve(f!, [0.05])

Printing sol shows the following:

Results of Nonlinear Solver Algorithm

* Algorithm: Trust-region with dogleg and autoscaling

* Starting Point: [0.05]

* Zero: [0.0673745373743581]

* Inf-norm of residuals: 0.000000

* Iterations: 4

* Convergence: true

* |x - x'| < 0.0e+00: false

* |f(x)| < 1.0e-08: true

* Function Calls (f): 5

* Jacobian Calls (df/dx): 5

We verify with the evaluation of sol.zero[1] using

f(r) = 1 - exp(-25*r) - 12.5*(1 - exp(-r)).

Life Cycle Savings¶

We apply the present value of future money to justify equipment purchases. Consider the purchase of newer, more efficient equipment.

The purchase requires a present sum of money, a cost.

The purchase represents a saving, or a benefit.

The cost occurs now, the benefit later. Compute the justification for the purchase of the new equipment. The approach to justify equipment purchases is called discounted cash flow analysis.

For each year of the projected life of the equipment, compute

\(+\) the projected savings,

\(-\) less costs for that year.

This gives the yearly net cash flow.

Discount the yearly net cash flow back to the present value.

Compute the life cycle saving:

\(+\) all net cash flow present values over the lifetime,

\(-\) less the first costs.

The important notions in a discounted cash flow analysis are first costs, return on investment, and payback period formally defined below.

We decide to invest in better equipment, which costs \(q\). The investment will save us \(p\) over \(n\) years. We compute the present value of \(p\) at discount rate \(r\):

against the cost \(q\) of the investment.

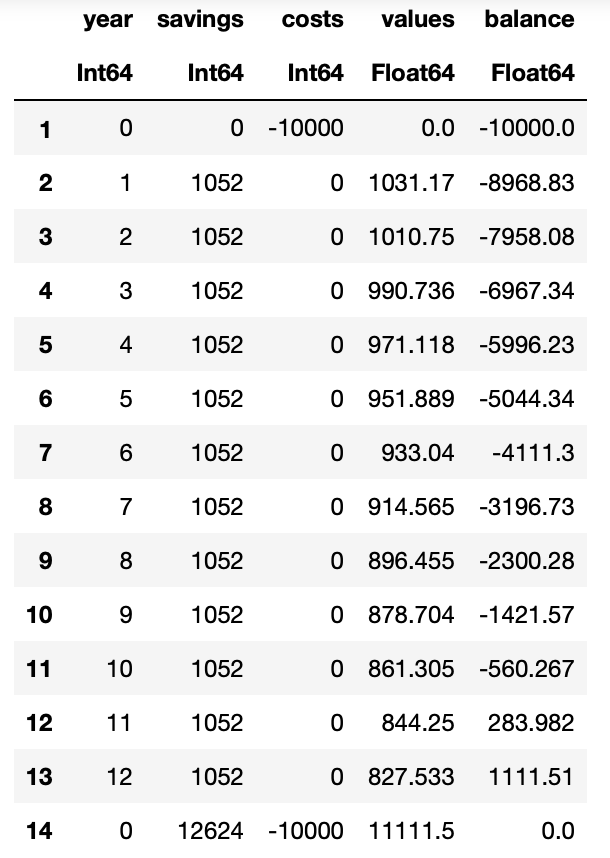

The definitions will be illustrated by a numerical example. We consider the purchase of new equipment:

The life span of the equipment is 12 years.

Each year, the new equipment will save \(\$1052\).

We use a discount rate \(r = d - i = 0.02\).

How much may the equipment cost to justify the purchase?

To answer this question, we use a dataframe, shown in Fig. 58 assuming the equipment costs \(\$10,000\).

Fig. 58 A dataframe to compute a discounted cash flow.¶

From Fig. 58 we see that in the eleventh year, we have recovered the cost of the investment, under the assumption that its purchase costed \(\$10,000\).

Proposals of Project Topics¶

Is a doctoral degree financially worthwhile? Is four years of study beyond the master’s to obtain a doctoral degree financially worthwhile?

Consider the following questions:

Does the added income throughout the career pay back

the cost of the education, and

the loss of income during the four years of study?

Is there is a difference between academia and industry?

Quality of a bachelors degree.

What is a good university education? Consider this question from the point of view of quality, using Taguchi Quality Control.

Focus on a particular major and define the expectations in financial terms. What is the expected start salary?

Define the parameters in the quality loss function.

Gather data and compute the quality loss coefficient.

Use public transport or your own car? For the daily commute, compare the cost of using public transport versus using your own car.

In your study consider the normal life span of a car.

The cost of public transport includes a fixed fare, subject to annual fare hikes.

The cost of a car includes not only the purchase price, but also taxes, insurance, fuel, repairs, and depreciation cost.

Answer the following questions:

What is the total saving of using public transport?

Explain how the annual increase in saving could be used to justify an annual fare hike, that is then also fair…

Buy a house or rent?

Suppose you receive a job offer which requires you to move to a different city. Should you buy a house or rent?

In your study consider a fixed number \(N\) of years, which equals the number of years of your job. The \(N\) can be used as a parameter.

Consider the costs and benefits of home ownership.

Consider the costs and benefits of renting.

Answer the following questions:

Given the transaction costs of buying a home, what is the minimum value of $N$ to make it worthwhile?

Home ownership is often cited as a protection against inflation. Consider the scenarios of low and high inflation rate and study the consequences of each in the buying or renting decision.

Should we colonize Mars?

What are the benefits of manned missions to Mars?

Make estimates of the financial investments (first costs) required to put humans on the surface of Mars?

What are the expected benefits to society?

As a point of departure for your study, gather historical facts and data of the moon landings. What were the costs and benefits of the moon missions?

Exercises¶

The solution to a nonlinear equation is in general not unique.

Plot the function

\[f(r) = 1 - \exp(-25 r) - 12.5 (1 - \exp(-r))\]for a suitable range for \(r\) to show that \(f(r) = 0\) for more than one value of \(r\).

For what value of the starting point does

nlsolveconverge to the other solution?Consider again the payout example of the lottery. Assuming the installment increases by \(3\%\) each year, at which rate does the break even point then occur?

Consider the payout plan of the lottery from the state’s perspective. What is the purchase price of \(q\) of an annuity that

pays out \(p/25\) for 25 years to the winner,

the remaining balance on the annuity grows at rate \(r\) annually.

Consider the numerical example on the discounted cash flow analysis,

assuming \(\$7,000\) as the purchase cost, and

inflation rate at \(i = 3\%\).

What is the return on investment for this problem?

Consider again the numerical example on the discounted cash flow analysis, assuming the cost of the equipment is borrowed

with a \(15\%\) down payment,

at an interest rate of \(5\%\), compounded continuously,

with a loan over 12 years.

Under these conditions of the loan, how much may the equipment cost to justify the purchase?

Bibliography¶

Charles R. MacCluer, Chapter 7 of Industrial Mathematics. Modeling in Industry, Science, and Government, Prentice Hall, 2000.

Peter Eichhorn and Ian Towers: Principles of Management: Efficiency and Effectiveness in the Private and Public Sector. Springer, 2018.